Investing and trading both involve putting money into financial markets, but they differ significantly in time horizon, objective, risk profile, and the skills they require. Knowing which approach fits your situation before committing capital saves both money and frustration. This guide breaks down every meaningful difference — including tax treatment under HMRC rules, the evidence on trading performance, and a self-assessment checklist to help you decide which path suits your life stage and schedule.

What is investing?

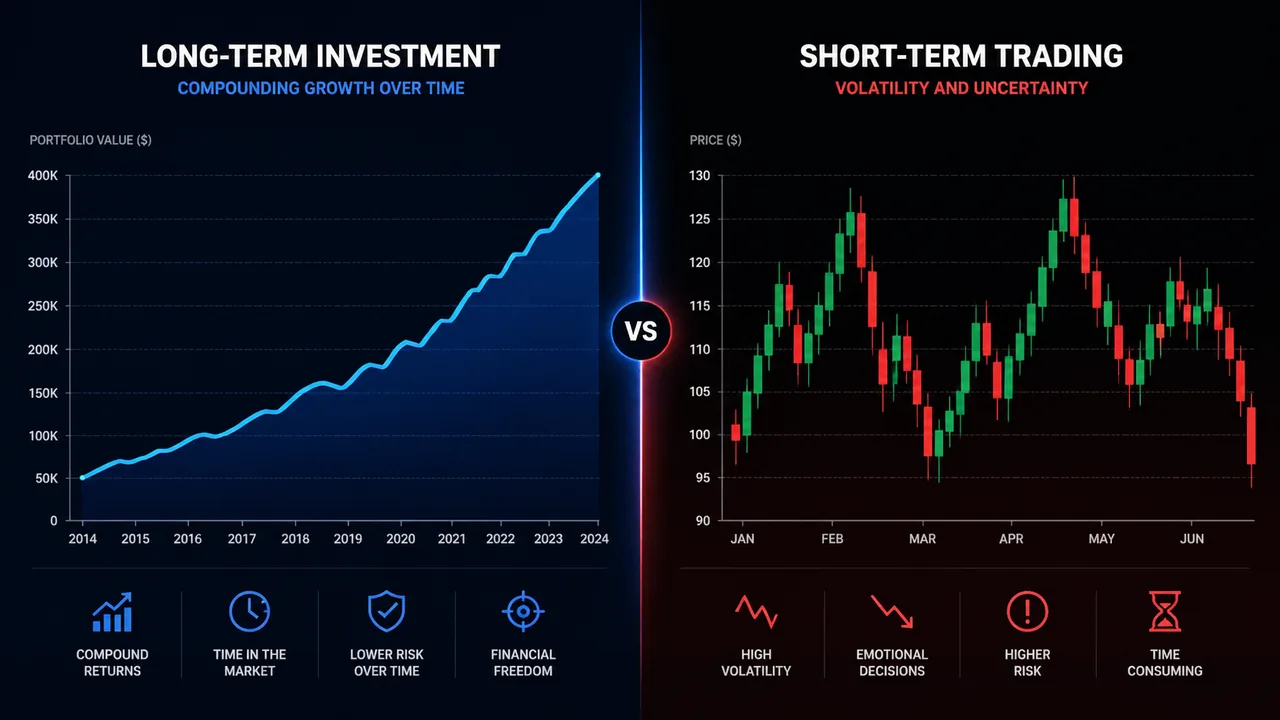

Investing means buying assets with the intention of holding them over a period of months or years to benefit from long-term growth and compounding. The underlying assumption is that over time, productive assets — shares in profitable businesses, for example — tend to increase in value. Dividends and interest payments along the way add to total returns.

An investor is generally not concerned with daily or weekly price movements. Short-term fluctuations are viewed as noise around a long-term upward trend. The investor’s task is primarily to select good assets at reasonable prices and hold them through market cycles.

What is trading?

Trading means attempting to profit from shorter-term price movements, from seconds (scalping) to days or weeks (swing trading). Traders analyse price patterns, economic data, and market sentiment to predict which direction an asset will move over a short timeframe. Profits come from many smaller moves rather than one large long-term appreciation.

Trading typically involves more active involvement, more frequent decisions, and higher transaction costs from spreads and commissions paid on each trade. It often uses leverage, which amplifies both gains and losses.

How much time does each approach require?

Time commitment is one of the starkest practical differences between trading and investing, and one of the most frequently underestimated by people new to financial markets.

Long-term investing can be largely passive once the initial setup is done. Opening an ISA, selecting two or three diversified index funds, and setting up a monthly direct debit requires perhaps four to six hours of work up front and a few hours per year thereafter — mostly to review allocations, reinvest dividends, and check that contributions are on track. Many investors check their portfolios monthly or even quarterly without it affecting their long-term outcomes.

Active trading is a fundamentally different commitment. Day traders typically spend several hours per day in front of charts, monitoring positions, watching economic calendars, and reviewing trades. Swing traders who hold positions for days or weeks require less constant attention but still need to check prices and news at least once or twice daily. Even part-time swing trading realistically demands five to fifteen hours per week of active attention. Skipping a session without closing positions first exposes you to overnight gaps and news events that can breach your stop-loss before you even see the trade.

This distinction matters enormously depending on your occupation and personal circumstances. A teacher, NHS clinician, or lawyer who works full-time has limited scope for active day trading during market hours without it affecting their primary income. Someone who works from home with schedule flexibility, or who is retired or self-employed, may have more practical ability to monitor markets. Honest self-assessment of how many uninterrupted hours you can realistically devote to trading per week is a prerequisite before choosing this path.

How much capital do you need for each approach?

Investing can genuinely start with very small amounts. Many major platforms — including Vanguard, Fidelity, and iShares — allow regular monthly contributions from as little as £25 to £50. The power of compounding means that time in the market matters more than the size of the initial sum. Contributing £100 per month for 30 years at a 7% average annual return produces a pot of approximately £121,000, even if you started with nothing.

Trading at small account sizes is considerably harder. The core problem is transaction costs. Each spread paid on a CFD trade represents a fixed cost that must be overcome before the trade becomes profitable. On a £500 account trading standard lot sizes, a single spread of £5 represents 1% of the account — a threshold that makes consistent profitability arithmetically difficult. Effective position sizing in active trading requires enough capital that each trade risk represents a small and consistent percentage of the total account. Most risk management frameworks for trading suggest risking no more than 1-2% of account value per trade. On a £500 account, that is £5-£10 per trade — limiting you to micro positions that generate small returns in absolute terms.

A common starting guide for active trading is a minimum of £1,000-£2,000, with £5,000+ allowing more meaningful application of position-sizing discipline. This is not a minimum to make large profits; it is a minimum to give risk management any practical effect.

Tax treatment: UK investing vs trading

The way HMRC treats your activity depends on what you do and which account type you use. The distinction is important enough to be a factor in choosing your approach, not just an afterthought.

For standard investing in shares, funds, and ETFs held outside a tax wrapper, profits on disposal are subject to Capital Gains Tax (CGT) above the annual exempt amount, which is £3,000 in 2025/26. Dividend income above £500 per year is taxed as dividend income at rates of 8.75%, 33.75%, or 39.35% depending on your income tax band. Both CGT and dividend tax can be avoided entirely by holding investments inside a Stocks and Shares ISA, which shelters up to £20,000 per tax year.

For CFD trading, profits are treated as capital gains in most cases rather than income. However, HMRC takes a holistic view of trading activity. If your trading is frequent, systematic, and generates a substantial portion of your income, HMRC may classify it as a trade — meaning profits would be taxed as income rather than capital gains, losing the CGT annual exempt amount. This is more relevant for professional or near-professional traders than occasional part-timers, but it is a genuine risk for anyone generating significant income from active trading.

Spread betting profits are generally tax-free for UK residents, as HMRC classifies spread betting as gambling rather than investment income. This is one reason spread betting remains popular with UK-based retail traders. However, losses on spread betting are also not deductible against other income, unlike investment losses which can be offset against capital gains.

Contributions to a Self-Invested Personal Pension (SIPP) receive tax relief at your marginal income tax rate, making pensions one of the most tax-efficient structures available for long-term investors. A basic-rate taxpayer effectively contributes £80 for every £100 that goes into the pension, after government top-up. A higher-rate taxpayer can reclaim additional relief through their self-assessment tax return.

Tax rules change, and your specific situation may differ. Always check the HMRC guidance on investment taxation or consult a qualified tax adviser. See also our guide to ISAs and tax-efficient investing for more detail on sheltering returns from tax.

What tools and knowledge does each approach require?

The knowledge base needed for long-term investing is different in kind from what trading demands, not just in degree.

A long-term investor primarily needs to understand company and fund analysis. This means being able to read a basic income statement and balance sheet, interpret a fund’s factsheet (total expense ratio, benchmark, top holdings), understand diversification and asset allocation, and grasp the long-term relationship between risk and return. None of this requires years of training. A motivated beginner can acquire a functional understanding in a few months of self-study.

Trading requires a substantially broader and more time-sensitive skill set. Technical analysis — reading price charts, identifying support and resistance, interpreting indicators such as moving averages, RSI, and MACD — forms the backbone of most retail trading approaches. Traders also need to understand order flow and execution, economic calendars and the market impact of specific data releases, risk management and position sizing, and the psychological discipline to follow rules under financial pressure. These skills are not impossible to learn, but they take considerably longer to develop to a level where they produce consistent results, and they require active practice rather than passive reading.

What does the evidence say about trading performance?

The evidence for long-term passive investing is well-established. Index funds tracking broad markets have outperformed the majority of active managers over decade-long periods, after fees. SPIVA data from S&P Global consistently shows that over 10-20 year periods, 85-90% of actively managed funds underperform their benchmark index after fees.

The evidence for profitable retail trading is far less encouraging. ESMA (the European Securities and Markets Authority) requires all CFD brokers operating in the EU and UK to publish the percentage of their retail client accounts that lose money. Across most major brokers, the figure sits consistently between 65% and 80% of retail accounts losing money over any given 12-month period. The FCA has cited similar figures in its own reviews of the UK retail trading market. Academic studies of individual retail trading accounts confirm this pattern: the majority of frequent traders underperform a simple buy-and-hold strategy even before accounting for the extra time they spend on the activity.

This does not mean profitable trading is impossible. A minority of retail traders do generate consistent returns, and some go on to professional careers. But the realistic baseline expectation should be that the majority of people who try active trading will, over a meaningful time period, lose money or at best match a passive index fund after far more effort. Understanding this before committing significant capital is more useful than discovering it through experience.

Which approach suits which life stage and occupation?

There is no universal answer, but certain patterns are consistent enough to be worth stating clearly.

Long-term passive investing suits almost everyone who has a time horizon of five years or more and some disposable income to save regularly. It is particularly well-suited to people who are employed full-time, have family commitments that limit discretionary time, or who are psychologically averse to watching short-term losses. Starting early — in your 20s or early 30s — gives compounding the maximum time to work. Starting later, in your 40s or 50s, still makes sense but increases the importance of consistent contributions to close the gap.

Active trading may be worth exploring for people who have a genuine intellectual interest in markets and price behaviour, have disposable time to study and practice, can set aside a ring-fenced sum they could afford to lose entirely without affecting their financial security, and who have the psychological resilience to handle frequent losses without abandoning their approach prematurely.

Many people find a combined approach works best: invest the majority of their capital in long-term positions and, if interested in trading, allocate a small defined portion to active speculation — often described as a “satellite” allocation — with money they can afford to lose entirely. This keeps long-term financial goals protected while allowing exploration of active markets without catastrophic downside.

Self-assessment checklist: trading or investing?

Use this checklist honestly before choosing an approach:

- Do I have at least five to ten uninterrupted hours per week to dedicate to studying and monitoring trades? If no, active trading is likely to be challenging.

- Can I afford to lose 100% of the capital I put into trading without it affecting my bills, savings goals, or emergency fund? If no, trading with that capital is inappropriate.

- Am I comfortable with the fact that 65-80% of retail traders lose money, and that I am likely to be in that group for at least the first year? If this is uncomfortable to accept, the psychological demands of trading will be difficult.

- Is my primary goal to build long-term wealth for retirement or a major life goal, or to generate income or excitement from markets in the short term? Long-term wealth building is better served by investing; short-term income generation or market engagement is the territory of trading.

- Do I have a regular monthly surplus that I can commit to saving regardless of what markets are doing? If yes, investing via ISA with a regular standing order is an obvious starting point.

- Am I willing to study technical analysis, keep a detailed trading journal, and spend months on a demo account before risking real money? If no, the preparation required for trading is unlikely to happen, making failure more likely.

Practical starting steps for each approach

If you have decided to focus on long-term investing, the steps are straightforward. Open an ISA with a low-cost platform such as Vanguard, iShares, or a comparison-listed provider. Choose one or two globally diversified ETFs rather than trying to pick individual stocks. Set up a regular monthly contribution, even a small one, to build the habit. Review your portfolio annually rather than reacting to daily price moves. See our guide to ETFs and index funds for specific fund suggestions.

If you want to try active trading, the preparation matters more than most beginners expect. Read widely about the specific market and approach you plan to use before committing any money. Open a demo account and practise for at least one to three months, keeping consistent records of your trades and the reasoning behind them. When you move to a live account, start with the smallest possible position sizes. Keep a trading journal from the very first day, recording both the trade logic and the outcome.

Related reading

- ETFs and index funds: the beginner’s case for passive investing

- ISAs and tax-efficient investing: what UK investors need to know

- Demo accounts: what they simulate and what they do not

- Position sizing: how to calculate the right trade size for your account

- Trading psychology: how fear and greed affect decisions

- Copy trading explained: how it works, which platforms offer it, and the risks

Frequently asked questions

Can I do both investing and trading?

Yes, and many people do. A common approach is to invest a core portfolio in diversified index funds aimed at long-term goals, and separately allocate a smaller amount to active trading. Keeping these in separate accounts makes it much easier to track the actual performance of each approach and avoid muddling the two strategies.

How much time does trading require per week?

Day trading typically requires three to six hours per day of active market monitoring during trading sessions. Swing trading, where positions are held for several days, requires daily check-ins of thirty minutes to an hour plus time for analysis outside market hours. Even part-time swing trading realistically demands five to fifteen hours per week including research, journal review, and strategy refinement. Long-term investing, by contrast, requires a few hours per year once the initial setup is complete.

What tax do I pay on trading profits vs. investment gains in the UK?

Investment gains on shares and funds held outside an ISA are subject to Capital Gains Tax (CGT) above the £3,000 annual exempt amount (2025/26), at rates of 18% for basic-rate taxpayers and 24% for higher-rate taxpayers on residential property, or 10%/20% on other assets. Profits from CFD trading are also typically treated as capital gains. Spread betting profits are generally tax-free. If HMRC determines that your trading constitutes a trade — based on frequency, professionalism, and the proportion of income it represents — those profits would be taxed as income at your marginal rate instead. Holding investments inside a Stocks and Shares ISA removes both CGT and dividend tax entirely within the annual £20,000 allowance.

Is day trading a realistic career for UK residents?

For a small minority, yes. For most people, no. ESMA data shows 65-80% of retail CFD accounts lose money over any 12-month period. Those who do profit professionally typically combine deep market knowledge, rigorous risk management, and often prior experience in institutional trading environments. The psychological demands are also significant — understanding the emotional side is just as important as the technical side. See our guide on trading psychology for more detail.

Which approach is better for building wealth over 20 years?

The evidence strongly favours low-cost passive investing. SPIVA data consistently shows that over 10-20 year periods, 85-90% of actively managed funds underperform their benchmark index after fees. Active trading introduces additional costs, tax events, and the high probability of underperforming a simple index fund. For most people building wealth toward retirement or other long-term goals, passive investing in diversified, low-cost funds is the approach with the strongest historical evidence. See our guide to ETFs and index funds.